Real estate tax in Slovenia 2026 – What homeowners need to prepare for

Slovenia will keep the same real estate tax brackets in 2026 as in 2025. This has been confirmed by the Ministry of Finance in its latest proposal for the annual revaluation rules. This article summarizes the key points for homeowners and investors and explains how the tax base, exemptions, deadlines and relief options work.

Who Pays Property Tax in 2026

Property tax applies to all natural persons individuals who own houses, apartments, garages or recreational properties, regardless of whether they live in them or rent them out.

Taxpayers include:

Residents and non residents

Owners and holders of usage rights

The tax is paid once per year, based on a decision issued by the Financial Administration (FURS).

Unchanged Tax Brackets for 2026

The Ministry of Finance decided not to change the tax brackets for 2026. This means that 2025 and 2026 taxation will be identical.

In previous years, the brackets normally increased annually, but this time the brackets remain fixed.

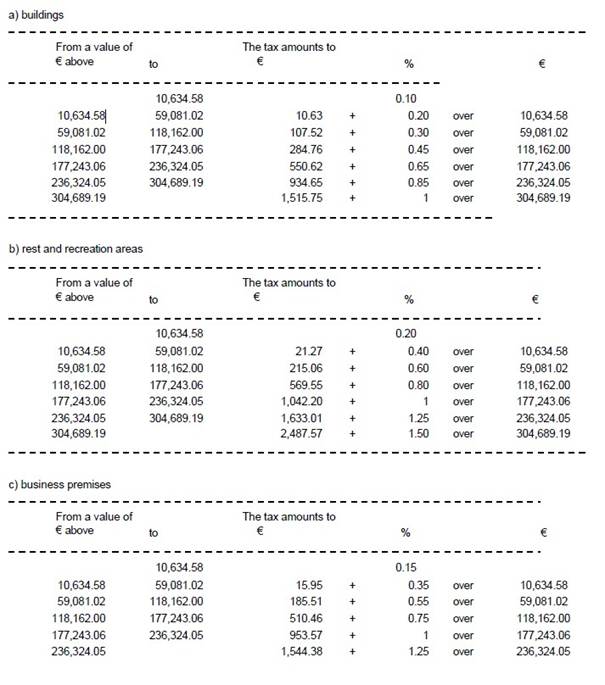

Tax Brackets for 2026

Below are the official 2026 tax brackets for:

Buildings

Rest and recreation areas

Business premises

The image you see in the post presents the exact values used for calculating property tax in 2026, including:

Minimum and maximum value ranges

Fixed tax amounts

Additional percentage rates applied on value above each threshold

These brackets remain unchanged from 2025 and will apply throughout 2026.

How the Tax Base Is Calculated

The tax base is the official value of the property. It is determined using the rules on valuation points, which depend on:

Useful area

Construction quality

Age

Additional property characteristics

Each property receives a value based on a points system multiplied by the value per point.

The 160 m² Deduction Rule

One of the most important elements of the system is the 160 m² deduction.

The tax base is reduced by the value of 160 square metres, but only if:

The owner, their close family member or the holder of usage rights lived in the property during the previous tax year.

Examples:

A 250 m² house used as a primary residence is taxed only on 90 m².

A property below 160 m² used as a primary residence pays no property tax.

Property Tax in Co Ownership

For co owned properties, everything is calculated proportionally.

Example for a 250 m² house with two equal co owners:

Each owns 125 m²

Each receives 80 m² of deduction

Each pays tax on 45 m²

Co ownership does not eliminate the tax obligation if the total property exceeds 160 m².

Who Must File a Tax Return and When

You must file a tax return when:

You buy a property

You build a new property, within 15 days of the occupancy permit

The tax return is filed at the local tax office where the property is located. FURS then issues a yearly decision with the amount due.

Failure to file is a violation that may result in a fine of 250 to 400 EUR.

Who Does Not Pay Property Tax

Full exemption applies to:

Residential properties up to 160 m² used as the primary residence

Agricultural buildings

Business premises used by the owner for their business activity

Residential buildings owned by farmers insured under agricultural income rules

Buildings protected as cultural or historical monuments

Buildings that cannot be used for objective reasons

Important: individuals with multiple properties are not exempt, even if some properties are smaller than 160 m².

Temporary Exemptions

Some taxpayers qualify for a temporary exemption:

First owners of new houses, apartments or garages – exemption for 10 years

Heirs who inherit new buildings – exemption continues under the same rights

Renovated buildings – exemption applies if the value increased by more than 50 percent

Reduced Property Tax for Large Families

Families with more than three household members living permanently in the property receive:

A 10 percent reduction for the fourth member

An additional 10 percent reduction for each further member

Deadline for Exemption Applications

Applications for exemption or reduced tax must be submitted to FURS no later than 31 January.

There is no official form. You must send a signed written statement. If the deadline is missed, the exemption will not be granted for that year.

Why Homeowners and Investors Work With SIBIZ

Property taxation in Slovenia includes legal conditions, valuation rules, reporting deadlines and exemption options. Errors can increase tax liability or trigger fines.

SIBIZ supports property owners and investors with:

Tax compliance reviews for property holdings

Assessment of exemption eligibility

Support with filings and documentation

Advice for foreign owners entering the Slovenian market

Clear guidance in English for long term planning

Our team works with foreign investors, homeowners, entrepreneurs, relocation clients and business professionals who want reliable and predictable support.

About SIBIZ

SIBIZ is a Ljubljana based advisory firm supporting foreign companies, investors, digital nomads and business professionals in Slovenia and the EU. We provide company formation, accounting, payroll, labour law guidance, relocation and immigration support and full ongoing corporate services.

Our specialists follow every regulatory update and translate complex rules into clear, actionable steps.

Slovenia’s business environment is poised for one of the most significant regulatory changes. The Slovenian Ministry of Economy, Labor, and Sports has submitted a draft proposal for the ZGD-10 amendment to the Slovenian Companies Act (ZGD-1) (EVA: 2026-2180-0009). Driven by the European Commission’s focus on global competitiveness and reducing administrative burdens, this landmark reform implements two key EU directives: Directive […]

A major regulatory change has officially gone into effect that will significantly impact transatlantic trade, supply chain logistics, and business operations across Europe. Effective July 1, 2026, the European Union has eliminated tariffs on the import of the vast majority of products originating in the United States of America. This historic step, announced by the […]

Slovenia’s national tax authority is bringing back a much-anticipated administrative relief measure this summer. The Slovenian Tax Office (FURS ) has officially announced a three-week tax holiday from July 27 to August 14, 2026. The initiative, which mirrors a successful pilot program from 2021, was introduced by the new head of the Slovenian Tax Office […]